Netease - Tailwinds Galore

Not investing in China is a mistake

Netease is one of my all-time favorite stocks.

It's been a prime example in my investment journey that you can achieve massive gains in industries that one understands best.

I worked in Gaming and bought my first shares in Netease in 2008 for a lowly price of around €16 per share. At today's share price, it has turned into an 18-Bagger!

The reasoning back then was simple. I was looking for successful PC/Browser-based gaming companies who had started the process of bringing their portfolio to the Mobile platform. In 2008, Netease also started publishing Blizzard's games in China. A company so obsessed with quality back then that it was a sign to me that Netease is a legit company.

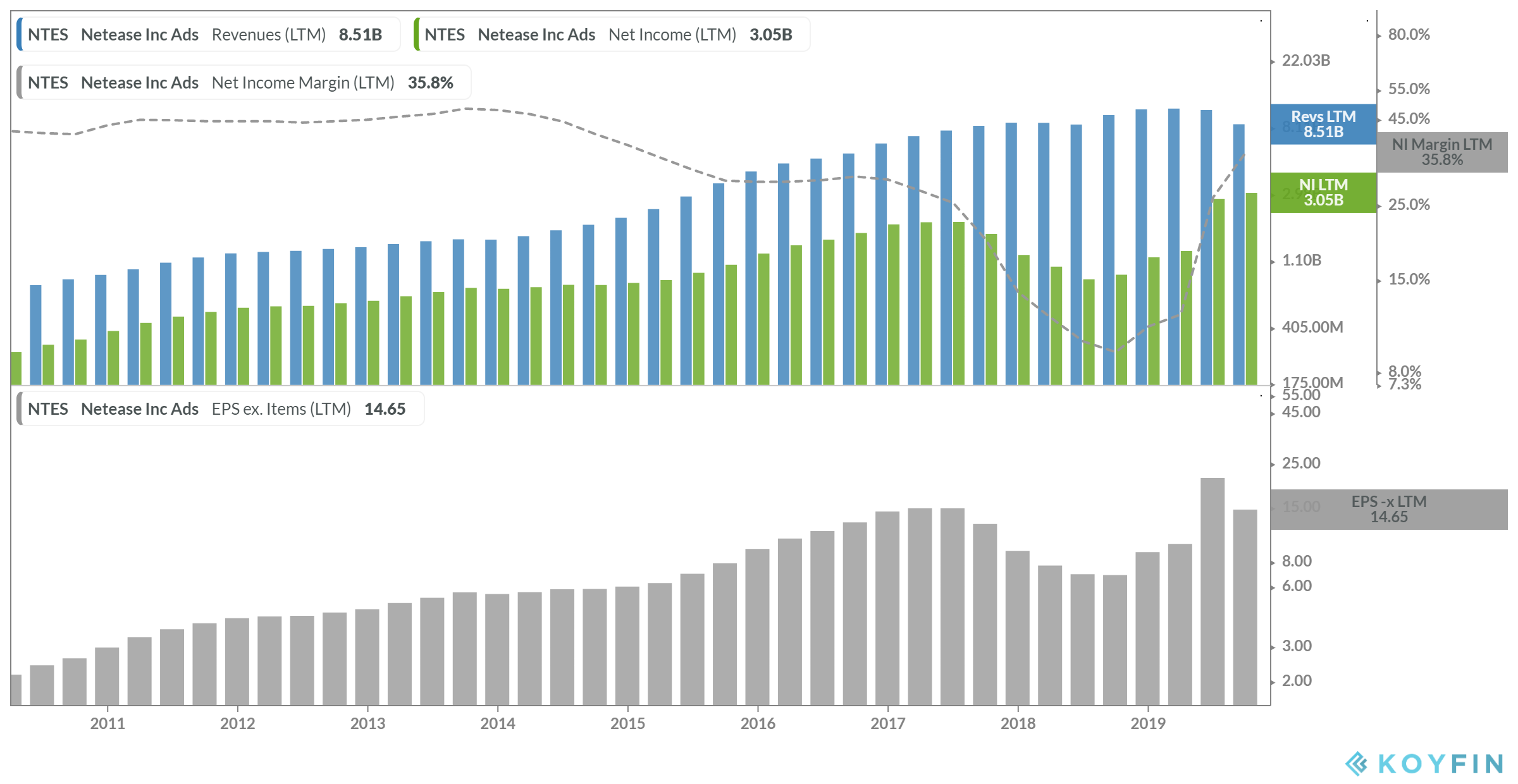

Execution has been superb over the years. Earnings per share have been growing consistently over a long period. The only hiccup worth mentioning is the 2018 period.

Netease doesn't provide forward guidance. I don't mind this at all. I like it when a company is spending more time executing rather than forecasting the unknown just to please analysts. As an investor, I want my regular updates, and I am getting those every single quarter.

While I rarely take profits on my winners, I have done so on multiple occasions in this case.

China is unpredictable, and the government gets involved in the day to day operations of companies. It is one of the most heavily regulated video game markets in the world.

A few recent examples,

Gamers under 18 are banned from playing online between 22:00 and 08:00

They are restricted to 90 minutes of Gaming on weekdays and three hours on weekends and holidays.

In 2018 the Chinese government established a Gaming regulatory body. They have to approve games for release. This resulted in Netease and Tencent not being able to bring games to the market for several months.

It would be a mistake not to invest in China, but I don't want a single Chinese stock to become too large a part of my portfolio. My current holding sits at around 5.5% of my overall portfolio. A size that I am comfortable with.

Netease Businesses

Netease has four business lines supported by long term tailwinds:

Online Gaming

Online Education

Cloud Music

Other Bets

In this article, I will focus on Gaming.

The majority of NetEase's profits are derived from its gaming business. In Q4, gaming revenues accounted for 74% of total revenues at a gross margin of 63.1%.

Games are developed very differently in China compared to the West.

As a product person, simplified to the core, I believe in the following:

Quantity: Take lots of shots

Quality: Take thoughtful shots

Consistency: Keep it up for a long time

Luck: A few favorable bounces are needed for mega successes

Netease delivers 1-3, even though the thoughtful shots are only achieved by throwing a huge number of people at a project.

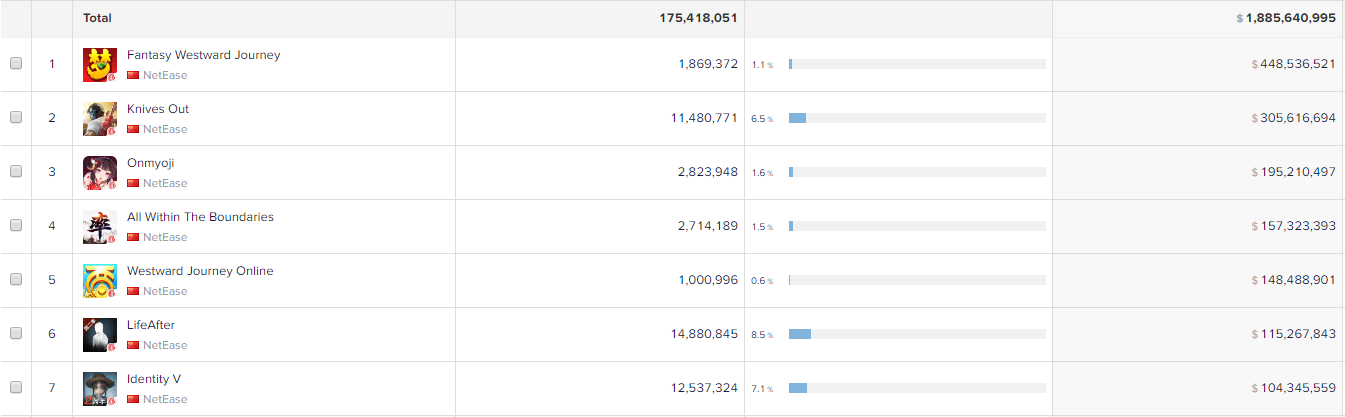

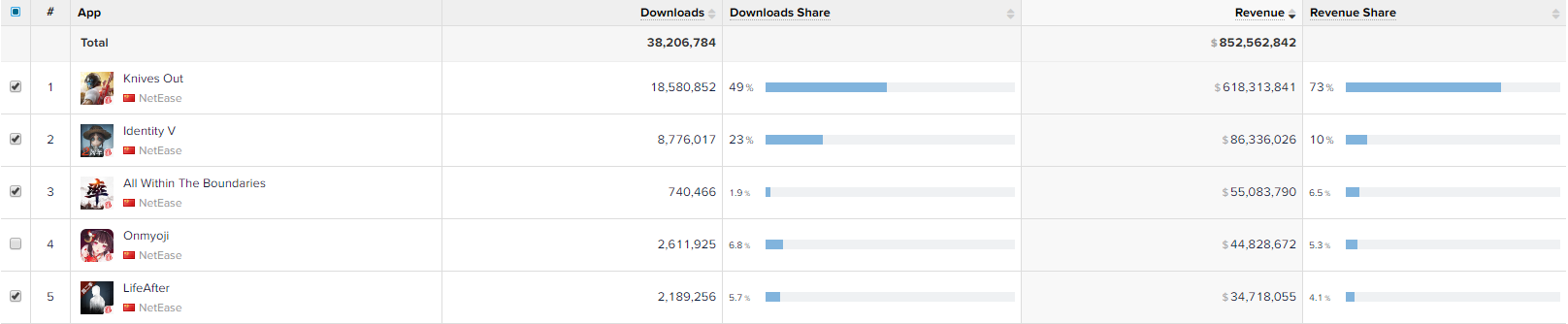

A good example is when PUBG rose to popularity; the game that popularized the battle royale genre. Netease released several clones in short succession, doubling down on the ones that stuck. This approach led to their second-biggest title in recent years, Knives Out. More on that later.

In the West, a small group of people will iterate towards the best result. Labor costs would never allow for such a shotgun spray approach.

It is a strong competitive advantage that Chinese companies have, particularly in games that are huge in scope and hard for smaller teams to replicate.

Where Netease differs from Tencent is that they have had no success in Western markets. They tried their luck developing games for the Western market themselves. These all bombed.

The current approach is to invest in Western developers, but they are only getting access to companies in the second row. The most notable one is probably their investment in Bungie. Tencent owns or partially owns many of the best Western companies in the Gaming space already.

Overall, it is too early to judge whether Netease investments will turn into meaningful success in the West.

Conquering the Western market aside, Netease has 7 Mobile games that generate more than $100m in annual revenue. That is a phenomenal track record.

Big In Japan

Beginning of 2018, one of their shots finally landed in Japan.

Within six months, Knives Out developed into a huge success story, generating more than $600m in revenue since the beginning of 2018.

Around the middle of 2019, several other games also showed strong signs.

Before 2018, Netease generated essentially no revenue in Japan. Today, it's closing in on $1b, and it's a fair assumption that they've cracked the Japanese market and will continue to release hit games there in the future.

Education and Other Bets

NetEase's other two business segments posted gross margins of 29.8% (Education) and 20.6% (Other Bets) in comparison. These have improved QoQ by 4% and 5.4%, respectively.

Online Education is growing strong, but only contributing 3% to overall revenue.

Other bets are contributing 24% to overall revenue. This includes innovative business lines such as streaming, cloud music, and legacy businesses, such as their email offering. The improvement in gross margin is being driven by Cloud Music and its Advertising business.

Going Forward

I've been a shareholder for 12 years and could very well see myself holding Netease another decade. While the high growth days are over, I expect them to continue to deliver market-beating returns in the future.

With the size of the Gaming business, temporary lulls are a risk, as it is not easy to develop the next hit game while keeping live operations for existing titles at a consistently high level. Long term, these are likely just short term blimps on the radar.

As an added bonus, Netease has a strong Browser/PC based portfolio. As everyone has been working from home during these times, this high margin part of their business is likely to see a medium-term bump.

The CEO still owns 45% of the company.

He has navigated the company through several changes and successfully expanded into new business areas numerous times.

He has delivered consistent revenue growth, profitability, and positive FCF for over a decade.

All business lines profit from our world becoming a more digital world.

Hit games can be operated for well over a decade, and they've consistently released new top performers and likely will continue to do so

Cracking the Western market in the future via one of their investments is not out of the question.

Their other business lines are growing, reducing overall reliance on the gaming business.

The China risk is priced in. At an EV/Sales of under 4, it is reasonably valued—Activision Blizzard sports an EV/Sales of over 7.