Pluralsight - Disrupting In-Person Training

Pluralsight - Disrupting In-Person Training

The mission is to democratize technology skills

Pluralsight is one of my more speculative investments.

At a market cap of around $2.5 billion, it's also one of the smaller companies in my portfolio.

Pluralsight IPO'ed in 2018, returning -8% since then. Towards the middle of 2019, the stock fell out of favor when growth concerns surfaced at a time when the public market also started to look for a clear path towards profitability.

I never invest in IPO's, as I like to see how a company is doing under the scrutiny of the public market. After watching the company for 12 months, waiting for the lock-up period to expire, I finally opened a position in my portfolio on 4th September 2019 at an EV/Sales of around 6.

What does Pluralsight do?

Pluralsight is a cloud-based technology skills platform that wants to help enterprises adapt and thrive in the digital age. It focuses on providing training for skills that are in high demand in today's world - Cloud, Big Data, Machine learning, to name a few. Anything Cloud-related is likely the most thought after skill right now with everyone forced into full remote work. It is smart to focus on these skills, as all of them are benefiting from secular tailwinds and high demand.

One might think that LinkedIn Learning, Coursera, Udemy, or even YouTube are the primary competitors.

YouTube has a lot of fantastic stuff available, but you have to find it. Within an organization, no CTO is going to tell you to go to YouTube for personal development in the workplace. It's unreliable content with no measurement of mastery. The likes of LinkedIn Learning are more structured, offer certificates, but have no focus. You can find courses on absolutely everything. The content is much broader.

Pluralsight has a clear focus on tech skills, targeting enterprises, and is aiming to build a product so convincing that every CTO wants to have it within their organization.

According to the CEO, the main competitors are in-person training conferences and instructor-led trainings, of which neither is currently possible.

Remote work and restricted travel, means that companies can no longer rely on traditional in-person training methods. In-person conferences and traditional instructor led training are two of our biggest competitors. Remote work and restricted travel mean close to zero current investment in those areas. Our platform provides personalized skill development, available anytime, anywhere and it helps team skill up faster and become more productive.

Pluralsight needs to seize the opportunity to work out how they can replace the in-classroom training experience for its large enterprise customers. Any businesses worth its salt will look for ways to continue offering personal development programs to its employees during these times.

Developing customized programs for large clients can change the game forever. The goal needs to be that none of them go back to in-person training post-crisis. The cost savings from reduced travel expenses would be the icing on the cake. I am convinced that the world will go down that path in the next 10 years, although it must be said that a good trainer can still make a huge difference today. In the future, I don’t see why an AI couldn’t be as good.

With everyone working from home, it is no surprise that Pluralsight management confirmed the positive impact on their business during their Q1 earnings call. The average amount of time spent on their training platform has increased 3x since the pandemic started.

Also, Pluralsight offered a "Free April" campaign that made its courses available for free the entire month. While primarily a brand-building exercise, some of those free users are likely to convert to paying customers (at a lower conversion rate).

Adoption of Online Learning

The digital transformation of our world has been accelerated at a rapid pace. Google and Microsoft both openly admitted this during their most recent conference calls.

Online Learning hasn't had an enormous breakthrough yet. It's also not exploding by vast amounts during the worldwide lockdown. What can't be denied, though, is that the adoption rate is pointing upwards, and I believe the best is yet to come in the next 5 to 10 years, which is what your time horizon needs to be with this kind of company.

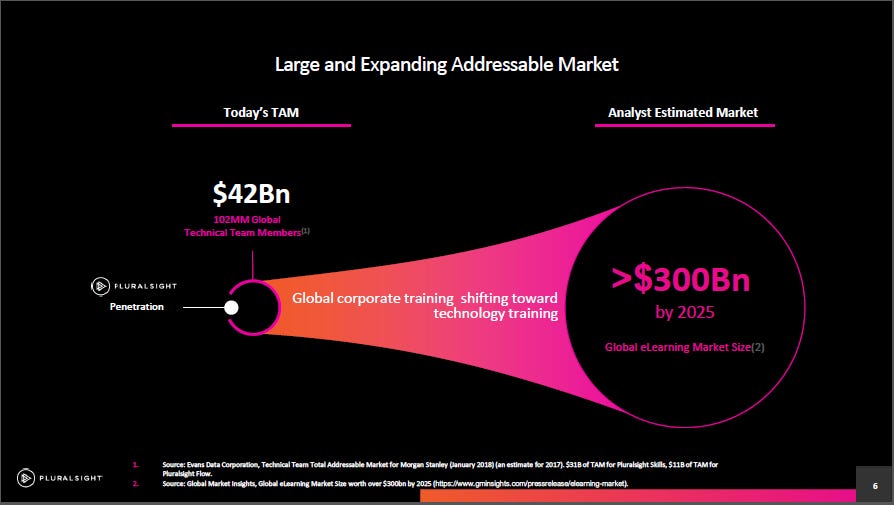

Pluralsight estimates their TAM to be $42 billion. $31 billion for Pluralsight Skills and $11 billion for Pluralsight Flow.

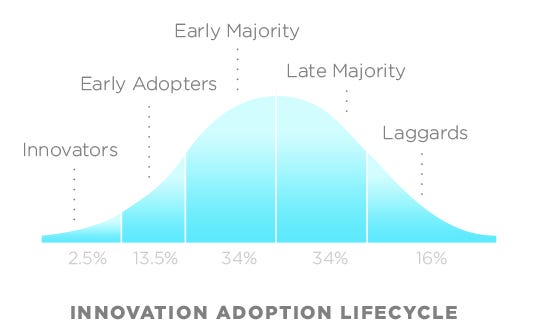

In an ideal world, you would always invest in a company before it's clear that their product is going to reach mass adoption.

Geoffrey A. Moore argues that while early adopters are okay with early-stage technologies, the early majority only accepts products that solve a problem they are facing.

Pluralsight is one of those companies. I would argue that it's past the stage of early adoption, yet it is far from reaching the early majority peak. That can all change over the next five years. Whether the TAM will be bigger than 300 billion by 2025 remains to be seen. My guess is as good as yours. I am certain that it will be significantly bigger than $40 billion.

Product Quality

The best formula for product usability and quality of online learning material hasn't been cracked yet. Pluralsight is best placed to crack the code and is currently offering the highest quality product already.

One particularly strong point of their overall strategy is that it places the CTO right at its heart. In 2019, they acquired GitPrime.

GitPrime is an analytics dashboard for development projects. It tracks code repositories on services like GitHub or Bitbucket, monitoring data points like user-by-user code commits over time, ticket activity, and how different team members tackle things like pull requests. Visually providing this data helps identify bottlenecks and highlights where teams are most efficient.

GitPrime was swiftly integrated into one of Pluralsight’s product offerings, Flow. It connects the learning platform directly with a codebase. A user is provided an individual training path based on the quality of their latest work.

That is superb usability that no other product on the market can match. Not even close. It removes friction and makes the entire experience simpler. The best products do precisely that.

With remote work likely seeing continued higher adoption post-crisis, leadership teams will look for ways to gain actionable insights on the productivity of their distributed workforce.

Whether Pluralsight's army of salespeople can sell this clear USP remains to be seen.

I am cautiously optimistic and hopeful that it becomes a compelling argument for CTO's, especially in large enterprises, as they get a complete overview as to what skills are covered and which ones are lacking in their organization.

Valuation

Pluralsight reported good Q1 results.

Revenue grew 33% y/y to $92.6 million, exceeding Wall Street's expectations.

The growth was almost entirely driven by business customers, with 89% of Billings coming from B2B customers.

Billings growth came in at 20% y/y. This is down from 28% in Q4 and needs to be watched closely.

Gross Margin improved four points to 81%.

Pluralsight announced $100 million in annualized cost savings. Not all will be realized this year, with 2/3rd coming from a hiring freeze.

Cash flow is trending positive for the year, there's enough cash on the balance sheet ($556 million) to whether any potential downturn.

Pluralsight guided lower towards $365 to $390 million in revenue for FY 2020.

At an enterprise value of $2.04 billion, the low end of the guidance represents an EV/Sales of 5.6x EV/FY20 revenues.

Seeing a Gross Margin of over 80% gives me confidence that Pluralsight will quickly trend towards sustainable earnings and positive cash flow as soon as the pandemic is over.

Long term, Pluralsight wants to achieve an Operating Margin of +20%. In the past four years, it has improved from -30% to -15%. Sales & Marketing costs will need to come down considerably in the future to achieve this. Right now, it's still about grabbing market share.

I consider Pluralsight to be fairly valued at around $18-$20 and will continue to hold my position.

If business fundamentals don't deteriorate in the future, I am likely holding on for 5-10 years.

As always, please do your own research before considering an investment.

You can subscribe for free below if you'd like to receive future updates directly into your inbox.