Portfolio Review - July 2020

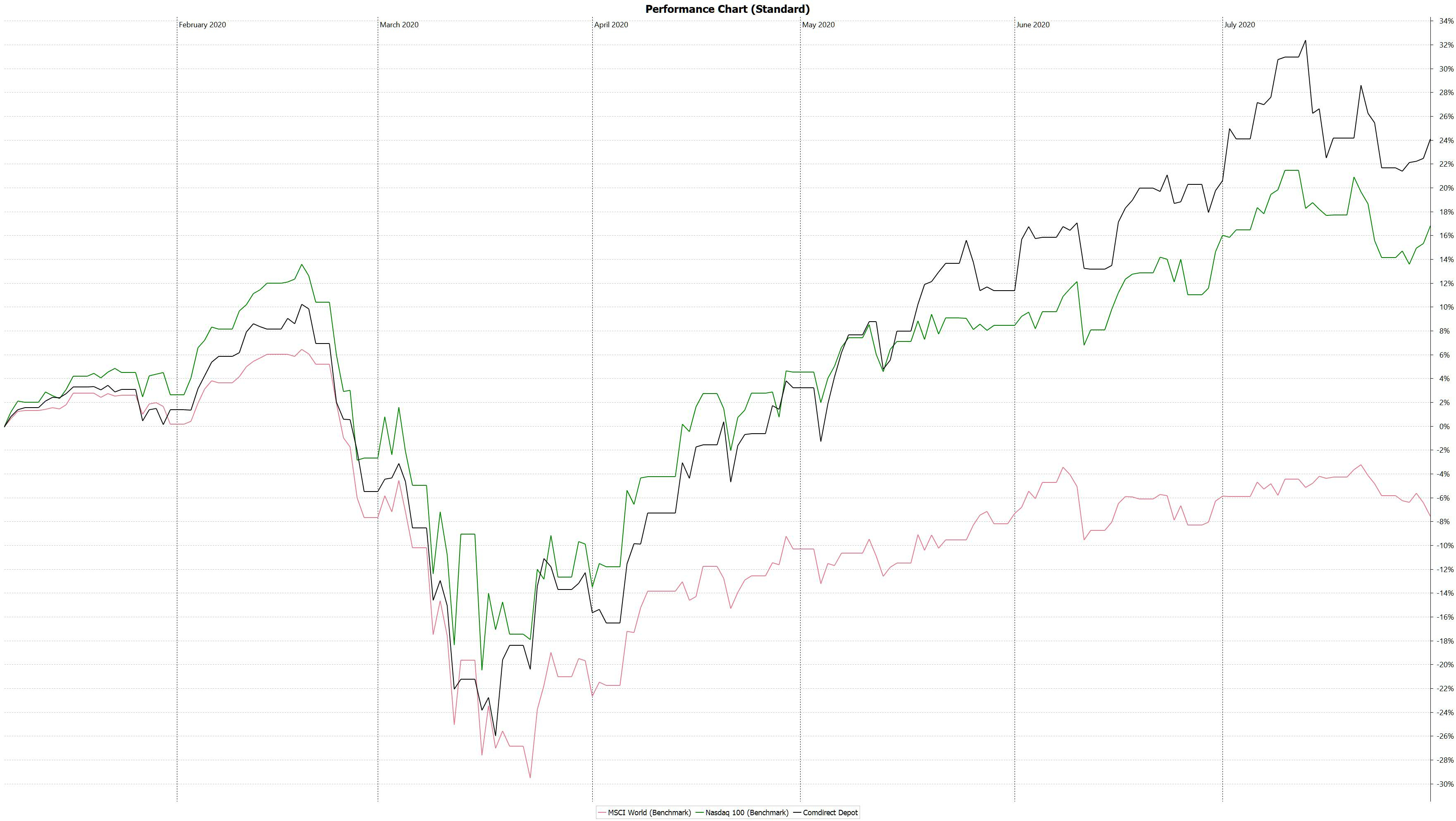

Total Return: 25.76% YTD (+7.3% vs Nasdaq 100)

My stock portfolio is built around one central thesis - the digitalization of our world. I believe that,

The digitalization of our world is 10% complete.

This megatrend will continue for at least another decade.

I believe that this trend allows for outsized returns. That's why I invest a significant portion of my net worth into individual stocks. If you're interested in my monthly portfolio performance, deep-dives, and analysis around my holdings, feel free to subscribe below!

2020 continues to be a great year for companies that are set up to benefit from the digital transformation of our world.

Around five years ago, I started to formulate my investment strategy around this central thesis on paper. That a pandemic would come knocking, accelerating this trend by years, I would have never predicted, and oh boy, is it exciting.

While my strategy has prevented me from entering "expensive" stocks, I am content with my return of 26% this year.

Other's are seeing 100%+ returns on every individual holding in their portfolio. That is not normal. Some of those companies are absurdly expensive. Time will tell whether those companies will grow into the valuations. Their business models are super profitable after all, and I do own some of the names where I think the future is rosier than what the multiples may imply.

The Nasdaq 100 has returned 19% YTD. An All-World Index ETF is sitting at -6.8% on the year.

I track against both, as I also invest a significant portion of my net worth passively.

The competitor in me wants to beat the Nasdaq100 as well, especially as I am shifting my portfolio more towards high growth companies, and they almost always happen to be Tech firms.

Portfolio & Performance YTD

Portfolio: 25.76%

Nasdaq: 18.97%

All World Index: -6.81%

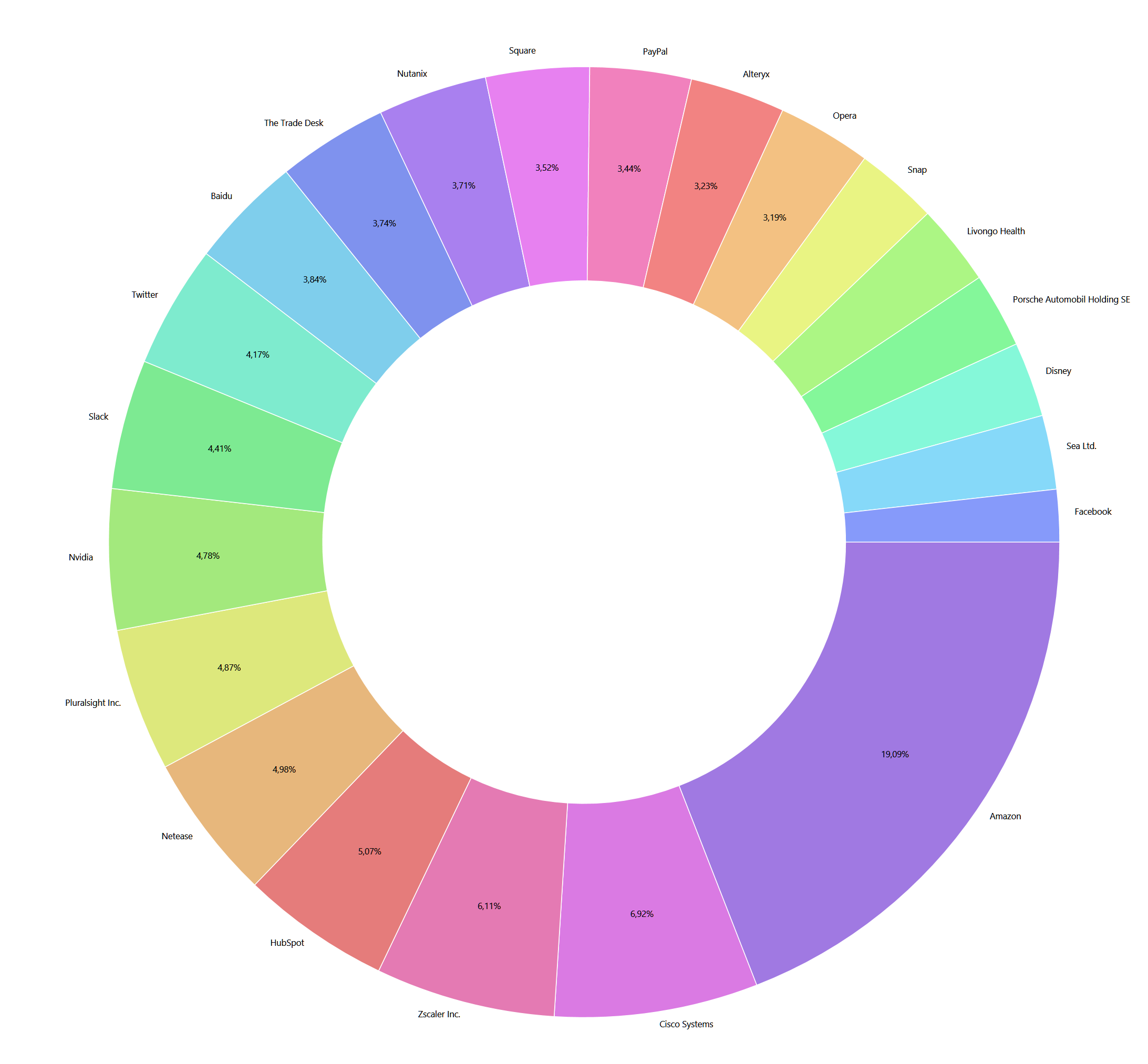

Current Portfolio - End of July

In July, I made a couple of moves.

New:

Sea Limited

I found Tencent too late and sold too early. Since those days, I've been waiting to find another company that could follow a similar path to success.

Sea Limited has a chance to become the Tencent of Southeast Asia.

Right now, they have business lines in digital entertainment and gaming (Garena), e-commerce (Shopee), and financial services (SeaMoney). Further business lines are on the horizon.

I expect the usual growing pains for a company that is predominately run by hungry, young people. There will be hiccups.

Up until now, I am super impressed by the execution and have opened a position that I will be looking to add to if execution remains strong in the next quarters.

Livongo Health

Education and Health are two areas that are ripe for disruption. Pluralsight is a company I own with regards to doing something relevant and innovative in the Education/Learning space.

After watching Livongo for a few months (and missing out on some insane returns), I am now on board with a starter position. Thanks to the pandemic, companies disrupting the health space have a much better chance of succeeding.

With a 70%+ Gross Margin, and a Rule of 40 of over 100%, this one is boasting impressive numbers. Valuation on an LTM basis looks stupidly expensive, but based on an NTM valuation; I am willing to open a position and monitor from here on.

Snap

I've always been intrigued by Snap as a company and waited several years to become an investor.

I now pulled the trigger on a starter position. The stock is not cheap, and this is a bit of a bet that their unique and innovative approaches in several areas come to fruition.

I always wondered who would be the first to bring over the Mini App approach that is so successful in China. Snap is taking this on. It's early days, but I see a chance that their entire ecosystem can turn into a powerful platform. That is what I am betting on and will be tracking it closely.

Added:

Slack

So far, this isn't playing out too well. While my first purchase at rock bottom prices looks excellent, my two additions since then have not been profitable.

The market hates the stock. I consider the whole drama around Teams to be noise.

Yes, Slack is not seamlessly onboarded into an organization. The value becomes apparent after you use it for a while, which by the way, also makes the switching costs higher.

The best companies are using Slack. The market is big enough for more than one player, e.g., Mac users building on AWS will never voluntarily use Teams over Slack. Big customer growth has been healthy every quarter, and if this isn't changing for the worst, I see no reason to question my investment.

This is a long term play with a great vision. Employees are behind the CEO, and customers love the product.

Trimmed:

Alteryx

Alteryx has to recognize revenue differently to your typical SaaS company with monthly recurring revenue.

I suspect that many will ignore this fact and misinterpret the next Earnings numbers if Corona puts a dent into new deals.

It is still a 3% position in my portfolio, and I am invested for the long term. I took some gains from the run-up as I needed cash for my new positions.

Sold:

Starbucks

It was always a small position that I've held for years. With my focus on higher growth companies, it had to go for merely that reason. The "boring" part of my portfolio is passive Index investing.

Overall, my portfolio now looks like this.

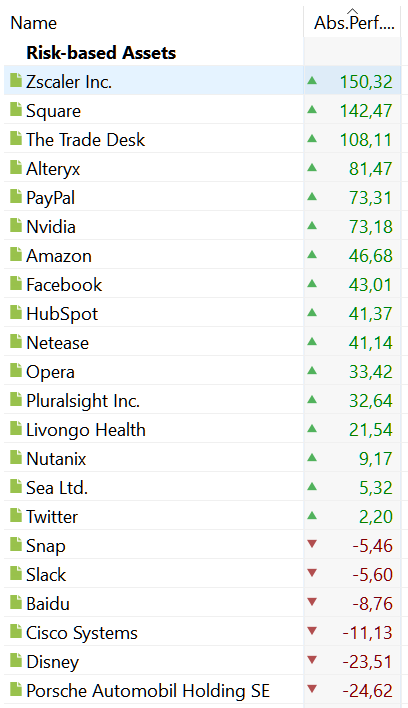

Top Performers - YTD

The Top 3 this year are ZScaler, Square, and Trade Desk. All three positions have increased by more than 100% this year.

The bottom two, unsurprisingly, are two companies struck by the pandemic, Disney and Porsche.

Baidu is a legacy stock that I believe will get a re-rate at some point. Slack and Twitter are two stocks that I think the market will eventually pick up on. I have high conviction in both.

Cisco will remain in my portfolio, as I don't have to pay capital tax gains on this tax, and I do believe it can outperform my passive index investment in the next couple of years.

Thank you for following my investment journey. I hope you found this useful and here's to an exciting August.

Thank you for reading!

Gr8 stuff. Thx