Portfolio Review - June 2020

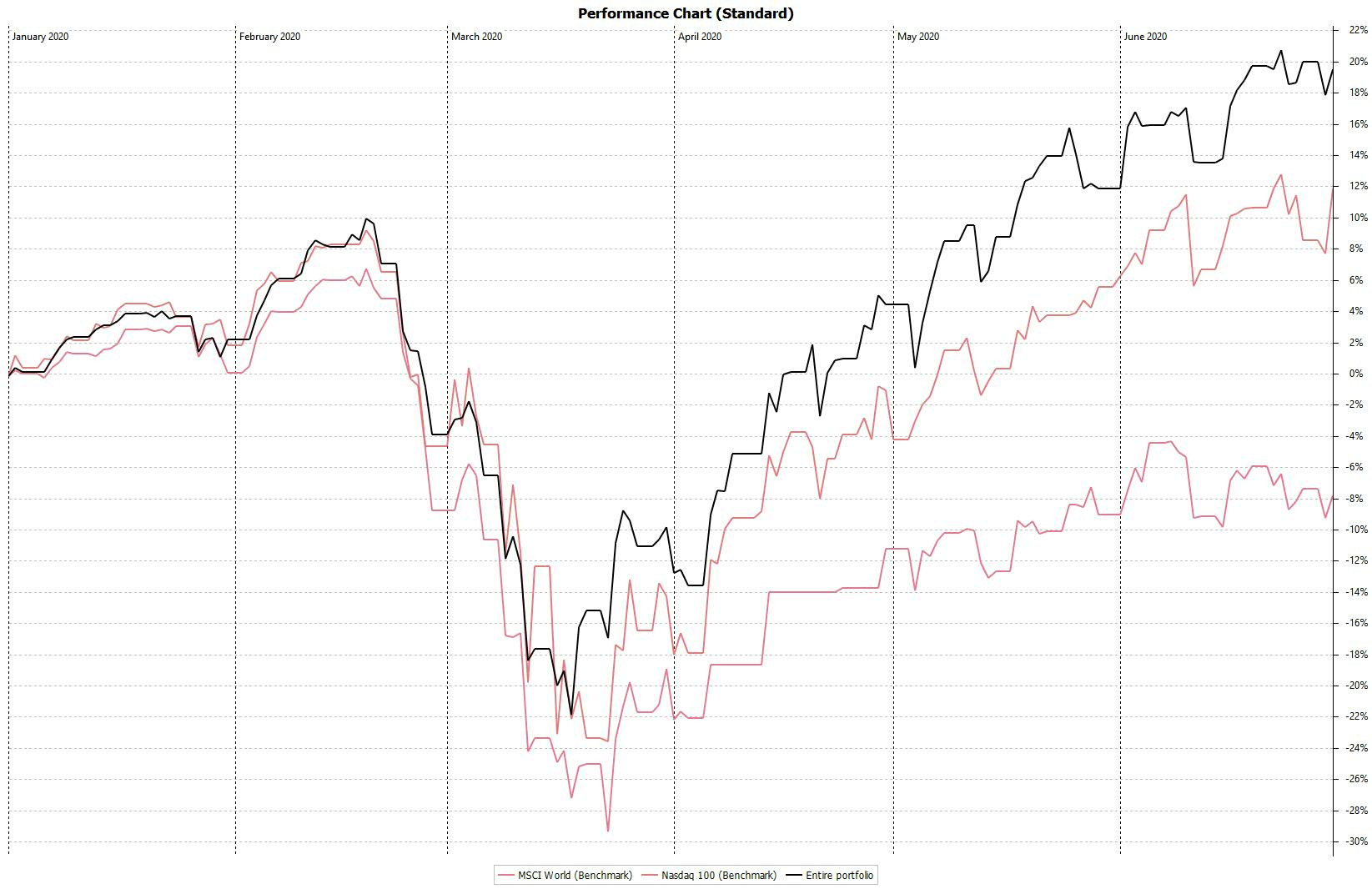

Total Return: 19.77% YTD (+7.66% vs Nasdaq 100)

My stock portfolio is built around one central thesis - the digitalization of our world. I believe that,

The digitalization of our world is 10% complete.

This megatrend will continue for at least another decade.

I believe that this trend allows for outsized returns. That's why I invest a significant portion of my net worth into individual stocks. If you're interested in my monthly portfolio performance, deep-dives, and analysis around my holdings, feel free to subscribe below!

2020 is a fascinating year.

2020 continues to be an incredible year.

My portfolio is now up 19.8% on the year, vastly outperforming an All-World ETF (-7.7%).

I have seen few people who primarily invest in Tech and High Growth stocks, benchmark against the Nasdaq 100.

I believe that this is the more accurate benchmark for a portfolio like mine. After all, I could simply buy that index and save myself a ton of work and time.

At +12.1% YTD for the Nasdaq 100, I am also beating this comparison, which I am thrilled with.

Some people see gigantic returns of +100% betting exclusively on SaaS stocks. Congratulations to them. My gains pale in comparison. With my approach, I can comfortably sleep at night, knowing that those SaaS returns are not normal, and anyone who is getting in at today's prices may be in for a rude awakening in the future when the slightest of hiccups surface.

As an investor, you face two risks:

The risk of losing money

The risk of missing out on opportunities

Going 100% into either direction is a mistake. One should not go 100% into Cash, and one should under no circumstances go 100% into High-Growth-Stocks.

You need to figure out the right level of offense vs. defense, just like a sports team.

For myself, I have a significant portion of my net worth in an All-World Vanguard ETF. I consider this my defensive portion of the portfolio as I have a time horizon of 30+ years. For others, defensive may mean holding a significant position in Cash, bonds, value stocks, or a combination of ETFs.

On offense, I do venture into high growth stocks who always tend to look expensive at any given moment in time. I consider this a full-blown attack. About the only thing riskier would be to get into angel investing, trade options, or speculate on currencies.

While I hope that my monthly musings serve as inspiration, and as a place to generate ideas, one should never blindly copy what I am buying/selling. My approach is tailored to my specific circumstances in life, and you need to come up with your own and act on your own beliefs.

On Valuations

I consider my portfolio fairly and, in the majority of cases, overvalued.

Let's do some basic calculations to illustrate this point.

The stock performance of Fastly YTD is absurd.

Everyone knows that Zoom has done incredibly well. They are up 272% YTD. Fastly tops this by quite a margin, up 324%.

The EV/Sales LTM is at 40x. NTM estimates are close to 30x.

Fastly quoted their Total Addressable Market (TAM) as ~18b, growing 25% every year.

Let's assume that Fastly can become the market leader, capturing 50% of the TAM - ~9b in yearly revenue. Applying a generous EV/Sales of 8 would mean that the future Enterprise Value is somewhere around $72b

Revenue in the last 12 months was $218m.

So this means that Fastly

has to become the market leader in a highly competitive market that isn't exactly known for pricing power

has to grow revenue from $218 million per year into $9 billion in revenue

has to avoid pricing wars at all costs

likely has to expand into other business lines successfully

In other words, they have to execute like hell for years to come, and you'd be looking at a 6x return. In 10 years, an attractive yield, if you believe that this can be achieved.

I would argue that there are other stocks with equally bright futures, with a more favorable risk/reward profile.

Portfolio & Performance YTD

Portfolio: 19.77%

Nasdaq: 12.11%

All World Index: -7.7%

Current Portfolio - End of June

In June, I again only made one move. I sold my entire stake in Oracle.

This holding is an excellent example of why copying someone's moves doesn't make sense. It's been a holding in my portfolio for almost 20 years, benefiting from some significant tax advantages that are no longer available to me for new investments.

Under normal circumstances, I would have sold Oracle a long time ago. As their growth prospects have slowed down tremendously over the last years, the underperformance vs. an Index was no longer acceptable, even when the tax advantage is added in.

That's why it had to go after almost two decades, and I will likely hold this cash position into the next earnings period.

At current valuations, you can expect me to make very few moves on the buying side, if any.

Additionally, I am contemplating selling my stake in Porsche, after the German management has once again proven, that they seem to be busy with internal power struggles, instead of focusing on catching up to Tesla. My original investment thesis may be broken. I will spend some time in July to think about it more clearly.

Top Performers - May

Opera finally showed some life after months of underperformance in my portfolio. The Trade Desk and Square round up the Top 3, again rewarding me with superb results.

Pluralsight took a breather. It ran up a lot, and this normalization doesn't worry me. It also has to do with their follow-on offering at $19.50, which put downward pressure on the stock.

Slack is a company that excites me massively. I believe many people miss the immense opportunity they have as one of the few "Work From Anywhere" plays. It's a position I plan on adding to. It is an expensive stock, but much more reasonable compared to many of the current darlings.

Thank you for following my investment journey. I hope you found this useful and here's to an exciting July. Thank you for reading!

If you liked this post from High Growth Investing by Christian Reshoeft, why not share it?