Portfolio Review - September 2020, -1.6%

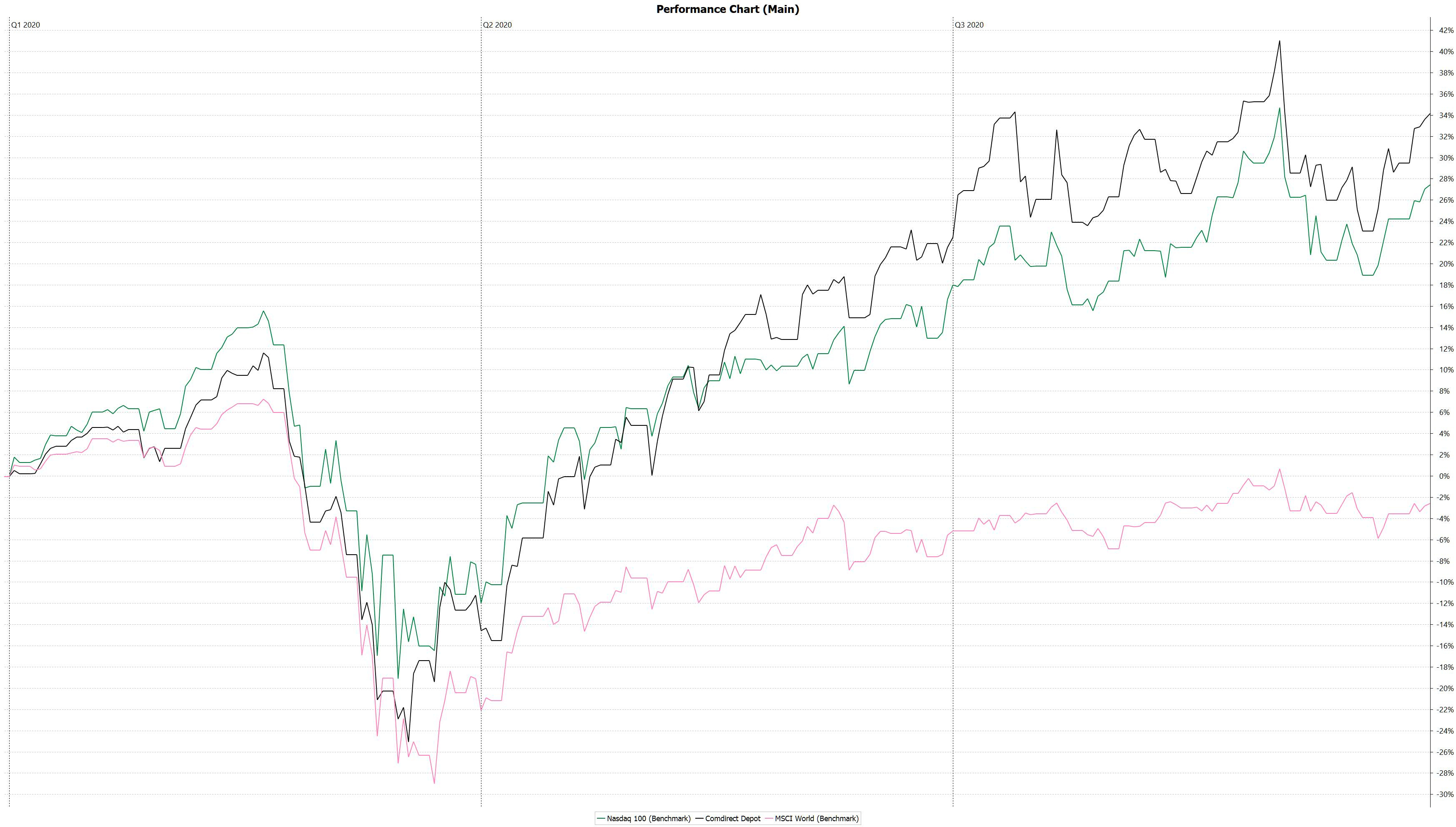

Total Return: 33.75% YTD (+6.56% vs Nasdaq 100)

My stock portfolio is built around one central thesis - the digitalization of our world. I believe that,

The digitalization of our world is 10% complete.

This megatrend will continue for at least another decade.

I believe that this trend allows for outsized returns. That's why I invest a significant portion of my net worth into individual stocks. If you're interested in my monthly portfolio performance, deep-dives, and analysis around my holdings, feel free to subscribe below!

Portfolio & Performance YTD

Portfolio: +33.75%

Nasdaq: +27.19%

All World Index: -2.74%

Some readers may be wondering why one should go through the hassle of investing in individual stocks when you can buy a Nasdaq ETF with around the same return this year.

6% outperformance may not seem like much, but a small percentage gain compounds into big gains over time.

$10,000 compounding at 10% for 10 years would result in $26,000.

$10,000 compounding at 16% for 10 years would result in $44,000.

It is worth it.

Most people invest more broadly than just into the Nasdaq, and that’s where you then have a chance to outperform the market significantly.

Top Performers - September

Snap and Twitter showed signs of life, and I continue to be bullish on Social Media plays in general.

The move towards E-Ecommerce will end up in more and more companies competing for users. Any platform that can supply these users will have an incredibly long growth tailwind well into the future. Hence, I am super bullish on Facebook, Snap, and Twitter.

Other stocks held up well during this volatile month, while Slack dropped heavily after the Q2 numbers, and Nutanix gave up a sizable chunk of last month’s gain.

Disney and Porsche are long term legacy holdings that I may replace with higher growth companies in the future. Both have recovered from the March lows but continue to be a drag on the portfolio.

Current Portfolio - End of September

In September, I made a couple of moves.

New:

Peloton

I’ve had Peleton on my watchlist since IPO. I had never initiated a position, as I had them pegged as slightly overvalued.

They smashed through all expectations, and certainly mine.

Even though I am getting in after the stock has increased 2x, I consider them to be reasonably valued after the fantastic quarterly results.

Apple launching Fitness+ is validation for the market, not competition. Direct competitors are well-funded startups such as Zwift, TheSufferfest, and TacX.

Their customer base has grown to over 500k subscribers, of which 317k are subscribing to the App.

Metrics were smashed across the board.

Their business model has clearly proven to be scalable and can be rolled out across international markets.

Docusign

The pandemic was a best-case scenario for Docusign.

Once you go paperless, you will not go back to signing and mailing various contracts around by hand.

It’s becoming a verb to “docusign,” even in Germany. Adobe’s moves need to be watched closely. They are way behind in terms of customer adoption, and for the time being, Docusign is the clear leader.

I’ve used the September correction to get in at an EV/Sales NTM of around 20x.

That is not cheap by any means, and you need to have a long term horizon of several years to allow the company to grow into that valuation.

Crowdstrike

Another company that is firing on all cylinders. ARR YoY growth of 87% at this scale is rare.

Furthermore, this is an incredibly efficient company, as seen by their incredible Rule of 40 score of over 100!

McAfee is planning an IPO, but these old legacy solutions are unable to compete with a company like Crowdstrike. The security market is being divided up between new entrants such as Crowdstrike and ZScaler.

Here I also used the September drop to open up a small position.

Added:

I added to my Facebook position during the correction. Some people hate the company; others love it.

What can’t be denied is that they reach a huge proportion of our world with their services.

Those can and will be monetized eventually, in ways that we perhaps can’t imagine today.

Their endeavors in E-Commerce are very likely to pay off, and Zuck is young. You can do worse than betting on his execution.

The company is also still reasonably valued after the September drop, in my opinion.

Slack

So far, I have been wrong on Slack. I am down 15% on my position.

Long term, I am as bullish as when I initially invested during the Corona crash and continue to add to my position.

Keep in mind that Slack is not a solution for short term problems. During the pandemic, executives needed to address short term problems first. How to deliver laptops to new employees, fix broken stuff, network security, and the security of employee’s devices.

Once the crisis is over, longer-term IT planning should normalize, and Slack’s enterprise business continues to be strong.

Last quarter they had 985 customers with an annual recurring spend of more than $100k, up 37% YoY.

Four of the six largest North American telecommunication providers are now $1 million customers on Slack. HSBC, a large European bank, doubled their spending.

This echoes the pattern in many other industries where the market leader chooses Slack.

New customer cohorts take a while to materialize. Q2 cohorts should contribute meaningfully in Q4 and into next year.

Slack Connect was mentioned in that it is emerging as a third sales funnel. While no numbers were mentioned, Butterfield hinted that its contribution to paid customers would only be growing.

Anyone joining through Slack Connect will also experience a vastly superior user experience. You already have people to talk to. The benefit for a business is immediately visible.

Fastly

Fastly is a small company that relies on a few customers, especially on a few large enterprise customers.

All the drama around TikTok was a classic example of what I would classify as noise.

That aside, their speed of innovation is impressive, and they are at the forefront of creating a new programmable platform.

The stock will be volatile, and I will likely continue to add to my position over the next months.

Sold:

Alteryx

This company is staying on my watchlist. I may re-enter as soon as I see that enterprise customers resume spending on their analytics solutions. 2021 comps should be favorable, but I expect this to be dead money in 2020 with further downside risk when Q3 numbers are reported.

Cisco Systems

I’ve held Cisco for around two decades. It was time to move on. I don’t want a dividend-paying slow grower in my current portfolio.

They were also affected by cutting down in enterprise spend on their various product offerings. Comps should also be favorable next year, but the company profile just doesn’t fit my current strategy.

I sold, raised cash, and deploy it into higher growth companies over the next weeks and months.

Overall, my portfolio now looks like this.

Top Performers - YTD

The Top 3 this year are ZScaler, Square, and Trade Desk. All three positions have increased by more than 100% this year.

Thank you for following my investment journey. I hope you found this useful, and here's to an exciting October.

Thank you for reading!

I want to share two links that allow you to invest alongside me.

Wikifolio:

If you are based in Germany, Austria, or Switzerland, then you can follow my Wikifolio. Once I publicize it, it would allow you to purchase a certificate through your broker that tracks my performance. Right now, you can watch it and can indicate whether you would be interested in investing.

EToro

My EToro portfolio, click here.

If you are based in Europe and are a user of EToro, you can copy my portfolio. This replicates all of my trades in your portfolio. Feel free to check it out if you like the thought of more free time and me doing all the work for you.