Slack - Work, Work, Work

Slack - Work, Work, Work

Slack has higher engagement than Facebook, Instagram, and YouTube

My stock portfolio is built around one central thesis - the digitalization of our world. I believe that,

The digitalization of our world is 10% complete.

This megatrend will continue for at least another decade.

I believe that this trend allows for outsized returns. That's why I invest a significant portion of my net worth into individual stocks. If you're interested in my monthly portfolio performance, deep-dives, and analysis around my holdings, feel free to subscribe below!

Slack has had a soft spot in my heart ever since I got to use the product.

Previously, I was a fan of Flickr, which Stewart Butterfield (Slack CEO) sold to Yahoo in 2005. Checkmark next to having a successful track record.

His next project was a video game called Glitch. They stopped development in 2012 and took their in-house communication tool, pivoted, and turned it into what we know as Slack.

I am unsure whether the name Slacks turns away some of the more conservative-led companies, as it could insinuate that it is just a big-time waster for employees.

In reality, it stands for “Searchable Log of All Conversation and Knowledge.”

The ticker symbol WORK gives the whole thing a playful combination, and it’s quite ingenious.

Launching in 2013, Slack quickly gained popularity with Tech companies, filling a void that Atlassian never managed to conquer. Their product, Hipchat, was deprecated, and Atlassian ended up investing in Slack in 2018, forming a partnership.

On its surface, Slack may seem like just another messenger platform. You have to use the product to grasp the full value that it can add to an organization.

You can integrate pretty much any cloud-based productivity and development tool into it, for example, the Atlassian product suite. This combination allows in-house and remote teams to work together efficiently.

As per their own words, it is a tool to create organizational agility. The combination of messaging and tooling integration is unique on the market.

For many, it reduces the number of emails. In reality, many conversations are just taken to Slack instead, and one has to be careful not to get overwhelmed by the number of messages. Especially as some users may expect instant replies, and others may feel the pressure to reply as soon as the notification pops up.

Competing products such as Basecamp argue precisely that. Slack, Microsoft Teams are the best way to stress out your team according to the arguably biased founder.

Of course, he’s not wrong. It takes discipline to use Slack well, and well-established company guidelines on how to use it.

Engineers, Product Managers, anyone in Tech will almost universally choose Slack. “To slack” has established itself in the vocabulary of all who use it. It may not be on the same level as “to google,” but perhaps it’ll get there one day.

I have been using Slack for a couple of years and could not imagine working without it anymore.

But I am getting MS Teams for free…

Everyone who is using Microsoft Office 365, and that’s a lot of us, is also getting Teams for free.

As much as Microsoft is promoting Teams, it hasn’t convinced companies who are using Slack to switch over.

My personal experience is that Slack has the weakest video call offering compared to Teams and Zoom. Many seem to agree, which is why numerous companies rely on a “Slack + Zoom” stack. Slack’s vision is, of course, grander than that. They don’t need to beat Zoom or Microsoft at the video game and instead are offering integrations into their product.

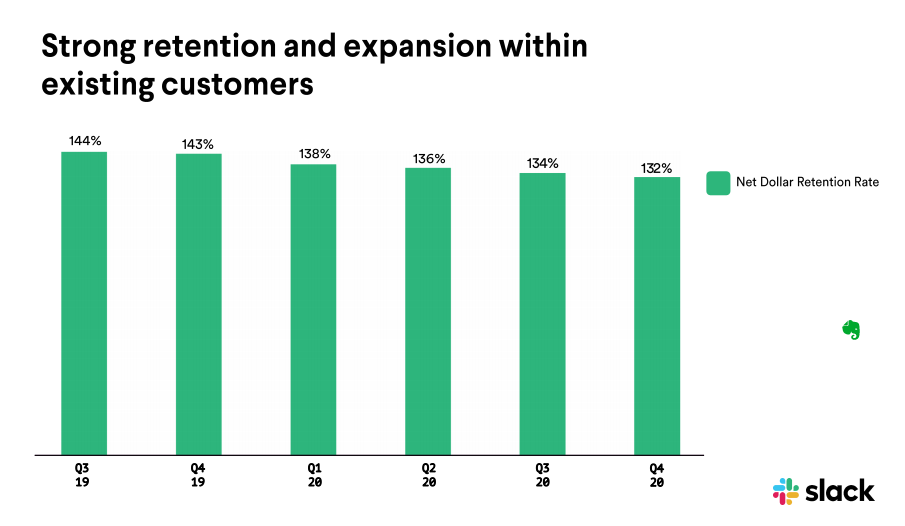

The numbers speak for themselves. The Customer Retention Rate for Slack has consistently been above 130%.

This number tells us that 110k existing customers, as per Slack’s latest filing, are spending 30% more compared to the prior year.

Not A Traditional IPO

Initial public offerings and direct listings are two methods for a company to raise capital. While many companies choose to do an IPO in which new shares are created, underwritten, and sold to the public.

In a direct listing, no new shares are created, and only existing, outstanding shares are sold with no underwriters involved.

Slack chose the latter. The CEO explained the reasons for this move here.

Was it a successful listing?

No.

The share price has been trending downwards ever since going public on the NYSE.

Why?

It went public at a very expensive valuation and had only recently dropped to levels where one could argue that it’s starting to become more reasonable.

If you have bought Slack at the very bottom for less than $20, congrats to you!

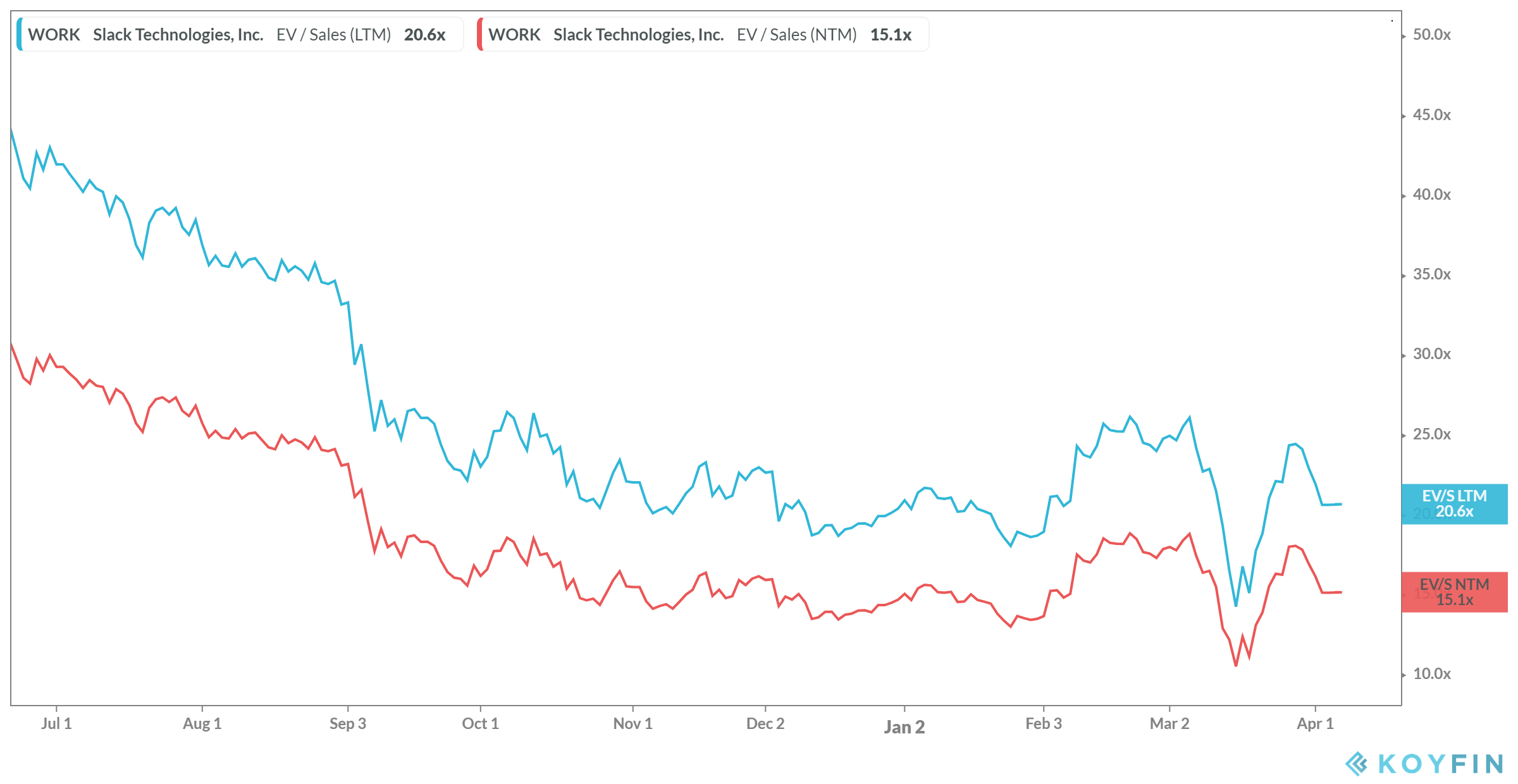

An EV/Sales LTM of 15 is likely to be a good deal considering that Slack is very likely benefiting from the current crisis.

Since then, it has recovered sharply, and you have to decide for yourself whether EV/Sales levels of 20 are still attractive.

The Bull Case

Revenue grew 57% to $630 million in FY20, guiding 35% growth to $852 million in FY21

Shortly after the most recent earnings call, Stewart Butterfield himself disclosed further significant growth on his Twitter profile, and how he is handling the current situation.

The above guidance is incredibly conservative, given how the world has changed after the earnings call.

Slack is a significant beneficiary of the work from home movement. This would have played out at a much slower pace without COVID-19, but now it’s accelerating the trend at an insane pace.

In the past, they gained 5000 new customers each quarter. They’ve already gained 7000 in a much shorter period.

Churn may be higher when the world hopefully goes back to normal in 2021, but by then, people will have gotten used to working from home, and this entire thing will play out as a net positive for Slack.

As an outsider looking in, Butterfield seems to be an exceptionally strong executor and world-class at understanding “product.” Best case, he turns out to be as strong as Zuckerberg at Facebook.

Slack is the platform that you open up when you boot up your computer. You don’t need anything else. If you do need it, you integrate it.

There’s only one way then, and that way is up.

The Bear Case

COVID19 provides a short term bump, with churn rising significantly in the coming months. Companies who are evaluating the product now, are not locked into the system yet. Switching costs are not high if you’ve only used Slack for 3 months, without any deep integrations. The current increase in customers will not translate to significant, long-term gains after the world has returned to normal.

They may point towards the weaker video solution which is more suitable for 1on1 conversations, and at best, small groups.

They may point at the poor search function and the considerable time it takes to effectively use Slack.

Slack recently released their biggest re-design to date, attempting to make things easier to use. Yet, all of these UI/UX improvements may not be enough to appeal to the broader audience that is undoubtedly checking out the product right now.

Companies may come to the conclusion that it is just another messenger, charging a high price. It’ll remain a tool that is solely used by Tech companies and more technically minded folks.

Even though it seems far away now, their prior guidance of less than 40% growth may become a reality again sooner rather than later. Due to high stock-based compensation, Slack is also nowhere near close to GAAP profitability. That would not be a good combination.

Final Thoughts

Let’s assume Slack will deliver much higher revenue growth, 55-65% or $976m to 1.04b in FY21.

At $28, the market cap is around $15.61 billion, resulting in an enterprise value of $15.08 billion.

Under these assumptions, the EV/FY21 comes out at 14.5x to 15.5x.

That is not a bargain anymore. Slack was definitely worth an investment a couple of weeks ago. The recent run-up has made the valuation a lot less attractive.

I’m definitely in the bull camp on the long term story, but I am not jumping in anymore at these price levels until more information is available.

The best comparison is likely Atlassian. Neither is profitable, but Atlassian is way ahead in terms of reaching profitability and has free cash flow margins of +30%, whereas Slack is guiding towards break-even. You pay roughly the same for both companies right now.

The next years will show whether Slack can develop into serious competition for the big players in the collaboration space, and I’ll be following closely.

Shoutout to the team at the Digital Leaders Fund, whose article on Slack served as my initial inspiration and starting point.

If you enjoyed this article, please do consider subscribing.

Thanks for your thoughts! Could you please explain how do you view the EV/Sales multiples of 15x or 20x as either cheap or attractive?